Anchoring bias is a straightforward behavioural bias that causes us to focus on a certain initial value and then make decisions with reference to it. Anchoring biases are pervasive. In this post we’ll discuss a number of anchoring effect examples to identify where they’re most prevalent and thus, hopefully, help reduce some of our silliness.

We’ll be covering the following:

Consider the nautical phrase ‘anchors aweigh’. This quite simply refers to the point at which an anchor starts to take weight as it’s pulled in, which in turn means the anchors are clear of the sea bottom and, therefore, the ship is officially under way. That’s sort of what we’re aiming for.

When was Albert Einstein born? If you don’t know the answer off the top of your head and you have no access to the internet, how would you answer this question? Perhaps you know that he was somehow associated with the atomic bomb development for the US (misquoted involvement aside, we’re just interested in the timelines). So that must have been before the US dropped the bomb on Hiroshima. And you know the Pearl Harbour and Hiroshima bombings were somewhere in the early 1940’s. When you think of Einstein in all those photos at the height of his career, you don’t see a young guy, but an older scientist, perhaps someone in their 60s? So, working back 60 years before 1940, our best estimate might be 1880.

The correct answer is 1879. Pretty close, huh? How did we work it out? We found an anchor to help us – the 1940s – and worked from there to arrive at an educated guess.

Whenever we need to guess something, we do this. It would be foolish to just pick a number off the top of our heads. We start with something we know and then use that to guide us into the unknown. Whether it’s guessing the number of people in Hong Kong, or the height of the Eiffel Tower – we use anchors. There’s no other way for us to do it. The problem though, is that we also use anchors when we don’t need to.

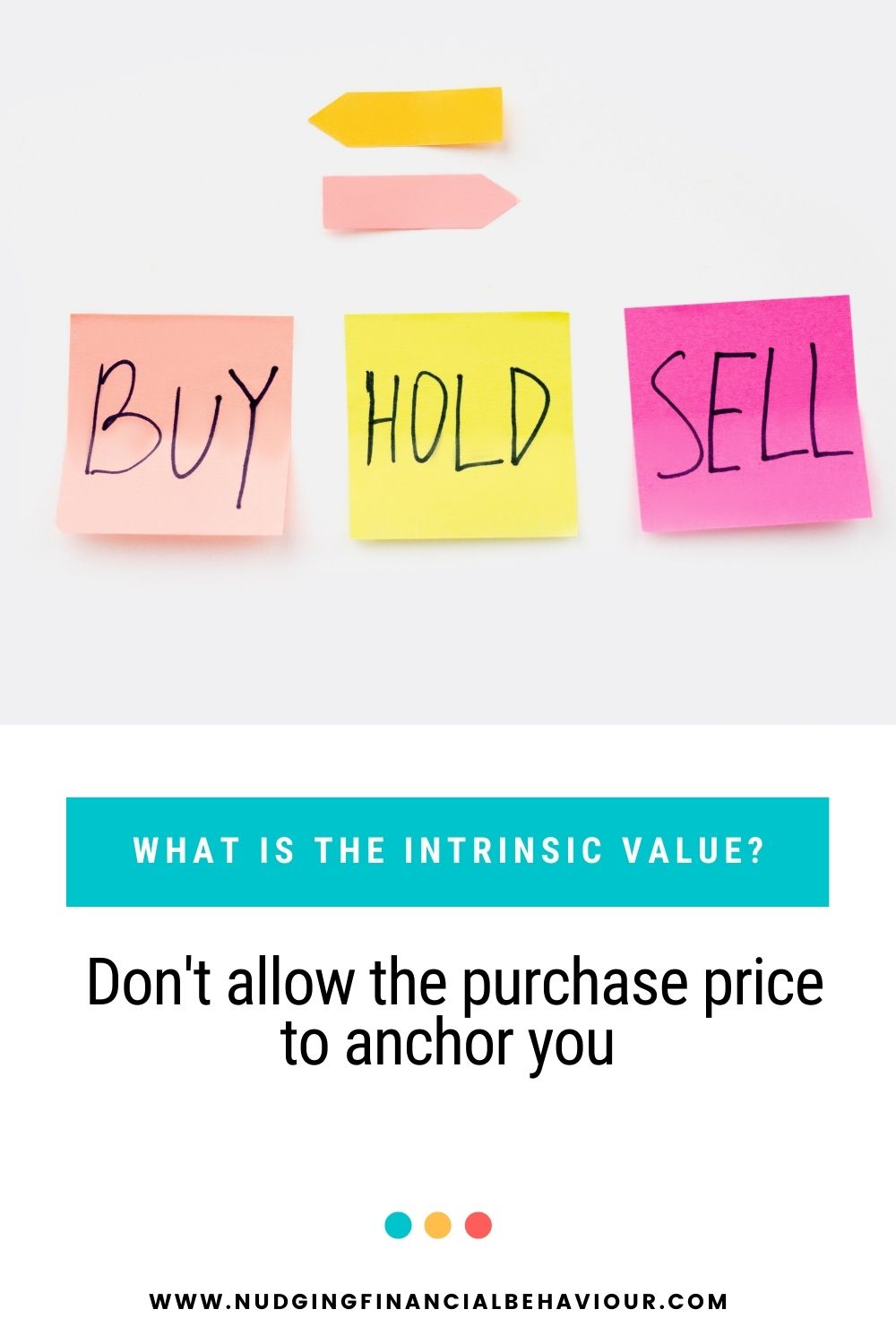

For an investor, a typical anchor is the original purchase price. And as we already know, we are unlikely to sell below that price (see loss aversion). But what about dividends? Basing your investment decisions on share prices at least directly contributes to the movement in those prices (a self-fulfilling prophesy). But how many of us invest based on dividends and are anchored to that, when it’s something we cannot even directly affect?

A final consideration is that of framing. Presenting the same situation in a different way using different frames, can anchor people in a certain way. This is where loss aversion creeps in again. Present a situation in terms of possible losses and people will likely take on risk to avoid those losses (risk-seeking). However, frame that same situation in terms of possible gains and we become risk-averse in trying to protect those gains. Anchors are ever-present in behavioural finance.

Whether you’re speaking to a real-estate agent, car salesman, or walking down the aisle at your local supermarket, beware of being anchored to a reference point. “Buy 4 for the price of 3!” That’s anchoring right there.

When you speak to your financial advisor, their recommendations are an anchor. And how does a company’s earnings announcement affect your assessment of their stock price? What’s important is to remember that you’re being anchored. Don’t allow your cognitive biases to influence your decision making, especially in negotiations.

We have no idea about most things and what they cost

Be careful of setting anchors with your investment returns. It’s fine to have a return goal, inflation + x%, but we must remember that we invest for the long term. If that investment return goal starts being a benchmark that you anchor all short term returns against you run into the risk of responding impulsively.

Anchoring is prevalent in everyday decision-making. What we should be mindful of is the need to differentiate between price and value. Forget about the ‘deal’ or what’s being punted. Make decisions based on the intrinsic value of the transaction. As we’ve seen with the Einstein example, some real knowledge can eliminate the uncertainty and ultimately the problem.

Want to pin this post for later?

Dr Gizelle Willows

PhD and NRF-rating in Behavioural Finance

The blog is written well